The Power of Having Savings Goals

By: Fidelity Viewpoints

Published: October 26, 2021

Key takeaways

- Identifying and describing your savings goals is typically one of the first steps in the financial planning process.

- Some of your goals may be deeply personal and unique. But there are other goals, like retirement or emergency savings, that everyone should have.

- Rest assured that it's normal for goals to sometimes change. If or when they do, you'll be able to adjust your plans.

You know you want to get ahead with your finances. Maybe you imagine this as feeling financially secure, as knowing that your family will always be taken care of, or as reaching a place where you feel like you can finally relax and enjoy your money.

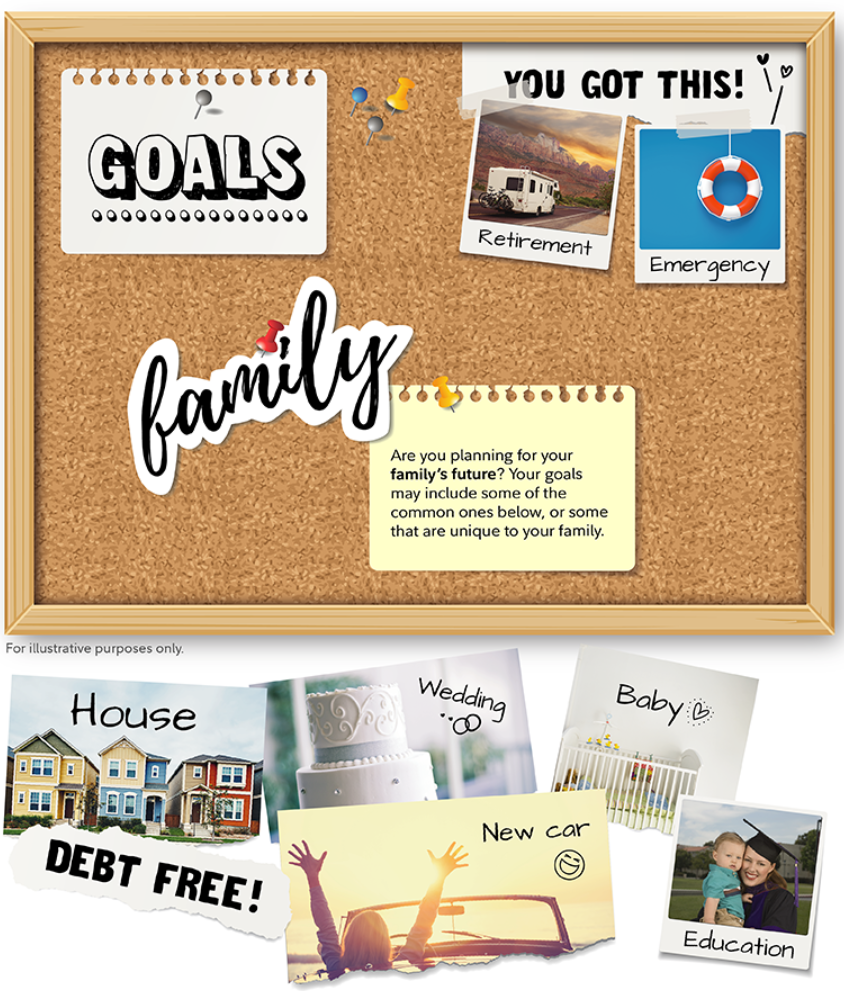

But if you dig a little deeper into this vision, what are the specific accomplishments that you see? Do you imagine owning your own home, or living completely debt-free? Maybe you picture helping a family member pay for college, or being able to afford a certain lifestyle in retirement.

These specifics are called your savings goals. And even if they still seem abstract or far off, it can be important to take the time to name them and think through as many details as you can. In fact, identifying your goals is typically one of the first steps in the financial planning process.

Your savings goals might not be your only financial goals. In order to start working toward your savings goals, you may need to check off other boxes on your financial to-do list first, like establishing a budget, paying off any high-interest debt, working on your credit score, and making sure you have sufficient insurance coverage and other financial protections in place. But once you're standing on a solid financial foundation, savings goals can be important milestones to help guide your progress over time. (Try our financial wellness checkup tool for ideas on strengthening your own financial foundation.)

Let's take a look at why savings goals are so important to successful planning, and how you can start to refine your own goals.

Why goals matter

Knowing your destination can help you map the best path to get there. Particularly for large or ambitious goals, it can be helpful to plan out the specific steps you'll take to bring your goal into reach. Identifying your savings goals can help you:

- Choose an appropriate investment mix. For some goals, such as ones that are many years away, you might be better suited with an aggressive asset allocation that provides the potential for higher returns but comes with higher risk. For others, such as nearer-term goals, you might need a safer investment mix even if it means lower potential returns. (Learn more about figuring out your risk tolerance and asset allocation.)

- Identify the appropriate account types. Saving and investing in tax-advantaged accounts can provide powerful benefits over time. But you need to choose an account type matched to your goal to make the most of the strategy and avoid potential penalties.

- Fine-tune your contribution amounts. Planning out your goals can help you figure out how much to contribute to each goal—whether you're crunching the numbers on your own or working through them with a financial professional.

- Measure your progress and adjust as needed. With an end-goal and plan in mind, you can keep regular tabs on your progress and adjust quickly if you start to get off track.

Finally, identifying your goals can give you a sense of purpose for all the hard work you put into your finances, and a feeling of accomplishment when you reach those mile markers you've set for yourself. After all, you can't cross the finish line if there is no finish line. When you have a clear goal, you'll have a way of knowing when you've arrived.

What you need to identify

So what does it really mean to identify your goals? As your vision of your future starts to come into focus, there are a few details you'll want to try to pin down for each one:

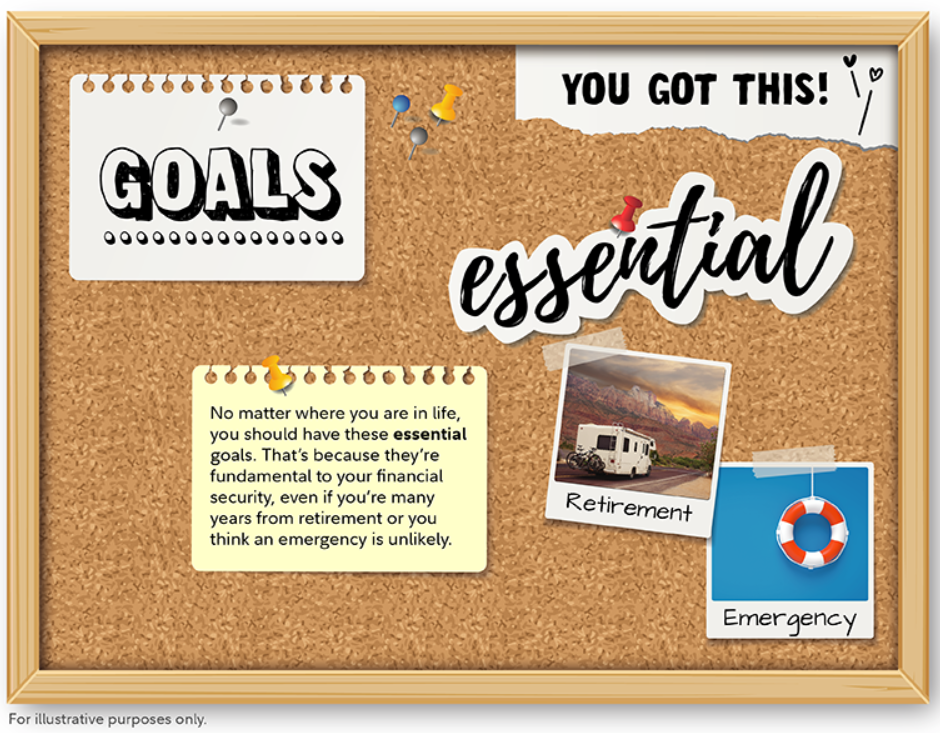

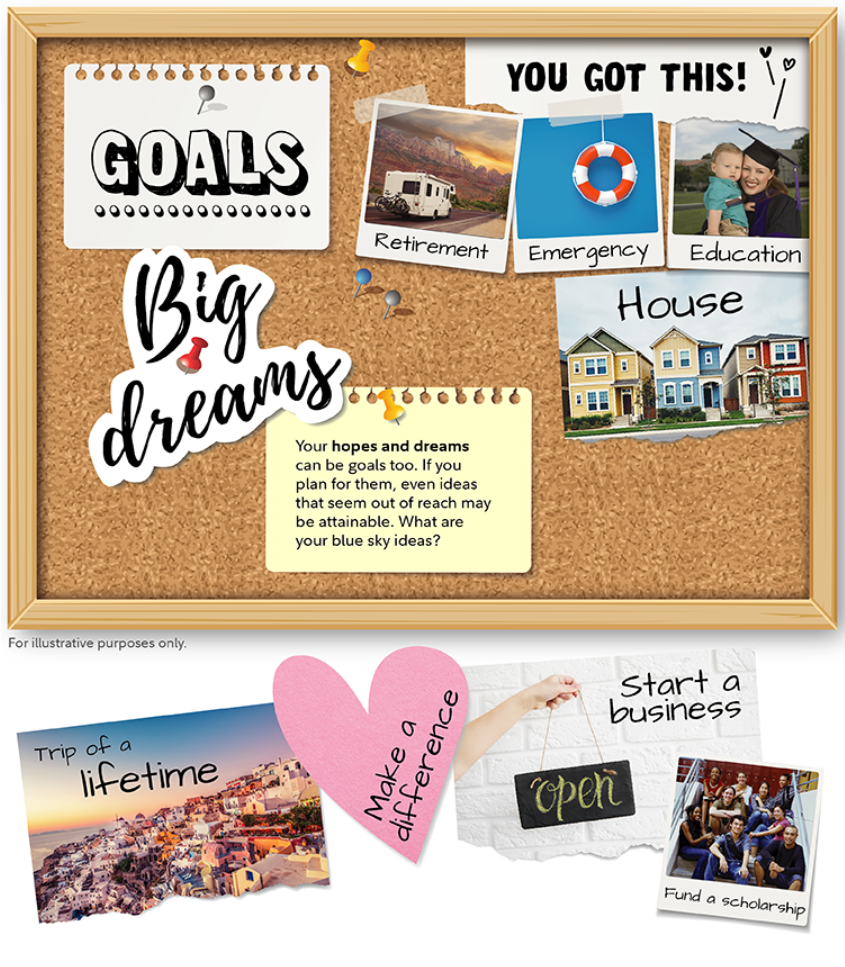

- What it is. Some goals are universal, like an emergency fund, while others may be unique to you. Coming up with yours can be a chance to express your values and to dream big.

- When it is. This is also called your time horizon, and it's important because it informs how much risk to consider when building your investment mix for that goal, plus determines how long you have to build up your savings.

- How much you'll need. Putting a price tag on each goal is a crucial detail that can help you determine the right savings rates, and help you track your progress to the finish line.

Consider writing your goals down, such as with our money goals worksheet(PDF), so you have a tangible reminder of what you're working toward. And know that it's OK at this stage to name some goals that feel more like dreams than sure things. After all, figuring out your goals is partly about defining your financial aspirations, and you'll be able to revise your list as you go along.

How to avoid getting stuck

For some people, making long-term plans is an exciting way to think big and build momentum. But for others, it can be paralyzing to feel like you need to map out the rest of your life milestones with any certainty.

Here are some common roadblocks you might run into as you try to identify your goals, and how to consider handling them:

- You're worried your goals might change. In fact, there's a good chance they will, and that's OK. If the past few years have taught us anything, it's that life is messy and unpredictable, and sometimes your priorities need to adjust. Do your best to think through your plans, but know that whatever you come up with will still only be a draft.

- You don't know how much you need. Picking price tags for your goals can be intimidating. Calculators and rules of thumb might help you start to narrow down your estimate, but many people find it helpful to work through the numbers with a financial professional. (Learn more about how much to save for retirement and college goals.)

- Your future is a blank slate. Maybe you truly aren't in the right place in life to choose concrete savings goals (beyond the 2 essential ones of retirement and emergency savings). In that case, you can consider adopting a catchall goal for now, such as "building wealth," until more definite plans start to emerge on your horizon.

Don't let perfection be the enemy of financial progress. And know that whatever your dream board ends up looking like, we're here to help.

Feeling inspired? Start building some momentum. After you write down your goals , consider setting up a savings goal so you can watch your progress. You can also explore how a managed account might help you keep on track with your investing plan, or set up an investing goal with the free Fidelity Spire® app.

Fidelity does not provide legal or tax advice. The information herein is general and educational in nature and should not be considered legal or tax advice. Tax laws and regulations are complex and subject to change, which can materially impact investment results. Fidelity cannot guarantee that the information herein is accurate, complete, or timely. Fidelity makes no warranties with regard to such information or results obtained by its use, and disclaims any liability arising out of your use of, or any tax position taken in reliance on, such information. Consult an attorney or tax professional regarding your specific situation.

Keep in mind that investing involves risk. The value of your investment will fluctuate over time, and you may gain or lose money.

This information is intended to be educational and is not tailored to the investment needs of any specific investor.

Fidelity Brokerage Services LLC, Member NYSE, SIPC, 900 Salem Street, Smithfield, RI 02917